Self-Employed & Small Business Owners in Georgia: Underwriting Hacks That Turn Complicated Into Approved

Navigating Mortgages as an Atlanta Area Entrepreneur

For small business owners and entrepreneurs in Georgia, the journey to homeownership can sometimes feel like an uphill battle. You work hard to build your business, and naturally, you take advantage of tax write-offs to minimize your tax burden. However, when it comes time to apply for a Georgia home loan, those same brilliant tax strategies can make your income look artificially low to traditional lenders.

As a Certified Mortgage Advisor based in Senoia, Georgia, I have helped countless self-employed professionals across Atlanta, Fayetteville, LaGrange, and Newnan turn a complicated financial picture into a resounding loan approval. The secret lies in understanding lender flexibility and utilizing specialized underwriting hacks designed specifically for business owners.

- Profit Add-Backs: Certain non-cash expenses, like depreciation, can be added back to your qualifying income.

- Bank Statement Programs: Alternative loan options that look at cash flow rather than tax returns.

- Custom Tailored Solutions: Working with a specialized mortgage broker who understands the nuances of self-employment income.

Insider Tactics: Profit Add-Backs and Bank Statement Programs

When traditional banks review your loan application, they often stick to a rigid set of rules that do not favor the modern entrepreneur. Fortunately, as an experienced mortgage broker in Senoia, GA, I have access to flexible underwriting guidelines that make a massive difference.

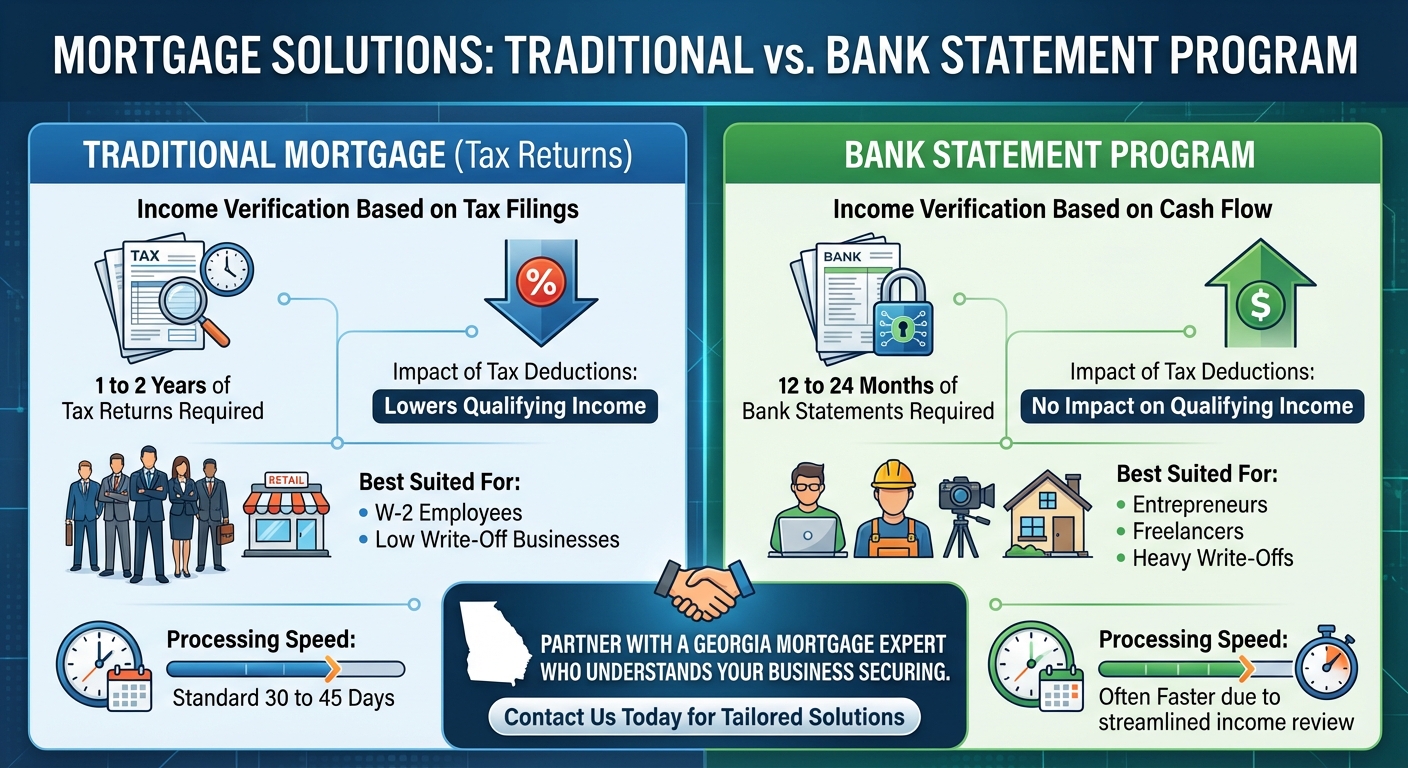

Profit Add-Backs are a powerful tool for small business owners. When underwriters calculate your income, they can add back specific deductions you took on your tax returns. Common add-backs include depreciation, depletion, amortization, and even certain one-time business expenses. This instantly boosts your qualifying income, increasing your purchasing power for that dream home in the Atlanta area.

If tax returns still do not reflect your true earning power, Bank Statement Programs are an incredible alternative. Instead of relying on W-2s or tax filings, lenders analyze 12 to 24 months of your personal or business bank statements. They calculate your income based on total deposits, giving a much more accurate picture of your actual cash flow. This is a game changer for freelancers, contractors, and business owners who have high revenue but heavy write-offs.

| Loan Feature | Traditional Mortgage (Tax Returns) | Bank Statement Program |

|---|---|---|

| Income Verification | 1 to 2 Years of Tax Returns | 12 to 24 Months of Bank Statements |

| Impact of Tax Deductions | Lowers Qualifying Income | No Impact on Qualifying Income |

| Best Suited For | W-2 Employees, Low Write-Off Businesses | Entrepreneurs, Freelancers, Heavy Write-Offs |

| Processing Speed | Standard 30 to 45 Days | Often Faster due to streamlined income review |

Partner with a Georgia Mortgage Expert Who Understands Your Business

Securing a mortgage as a self-employed professional does not have to be stressful. The key is working with a lender who knows how to present your financial story in the best possible light. Whether you are looking to purchase a new home in Fayetteville, refinance a property in LaGrange, or tap into your home equity, having a Certified Mortgage Advisor in your corner is invaluable.

My approach is holistic. We will review your unique financial situation, explore all available Georgia mortgage programs, and identify the exact underwriting hacks needed to secure your approval. By focusing on your true cash flow and utilizing lender flexibility, we can turn your complex income into a straightforward path to the closing table.

If you are ready to stop stressing over tax returns and start shopping for your next home, it is time to get pre-approved with a strategy built for entrepreneurs.

Q1: Can I buy a home in Georgia if I have only been self-employed for one year?

Yes, while many traditional lenders require two years of self-employment history, there are specialized Georgia home loan programs that allow for just one year of self-employment, provided you have a strong previous work history in the same industry.

Q2: What are bank statement loans and how do they work?

Bank statement loans are alternative mortgage programs designed for self-employed borrowers. Instead of using tax returns, lenders calculate your qualifying income based on the total deposits made into your personal or business bank accounts over a 12 to 24 month period.

Q3: Will my business tax deductions stop me from getting a mortgage?

Not necessarily! As an experienced Senoia mortgage broker, I can use underwriting tactics like profit add-backs to add non-cash expenses, such as depreciation, back into your qualifying income to help you get approved.

Q4: Do bank statement loans have higher interest rates?

Bank statement programs may have slightly higher rates than conventional loans because they carry different risk profiles, but the flexibility they offer makes them highly valuable for small business owners who cannot qualify using standard tax returns.

Q5: How do I start the mortgage process as a small business owner in the Atlanta area?

The best first step is to get pre-approved. Contact Jeff Wilmoth, your local Certified Mortgage Advisor, at (404) 597-5662 to discuss your specific financial situation and discover the best loan options for your needs.

Get Pre-Approved for Your Georgia Home Loan Today